'Liquid Assets'

Fine wine and liquor have cratered amidst rising retail prices and sticky inflation.

TL;DR: 2025 could be a “good year” for wine. Economically, the wine industry has suffered in the 2020s. Luxury good intrinsic values are down despite retail prices remaining high. Tech increasingly plays a role in wine and liquor industries. Valuations are cheap, but could get cheaper.

The trough

Nearing the bottom of the barrel.

As harvest season draws to a close, early indications suggest that 2025 could be a strong year for wine quality, while yield quantities continue to be varied due to weather and higher input costs. After a disastrous 2024, this year’s promise could bring much needed relief to consumers and producers alike.

Since pandemic drinking and inflation spikes, wine cellar values have broadly declined back to pre-covid levels based on the Liv-ex (London International Vintners Exchange) 1000 bottle market index1.

As an asset class, investment grade wine suffered a significant correction in recent years along with whiskey, watches and other luxury wares. These high-end discretionary goods peaked in early-mid 2022, then sold off rather aggressively given rising rates, plunging Chinese demand and reversal of covid-era froth. Liquidity across collectibles markets was not deep enough to withstand the elevated selling.

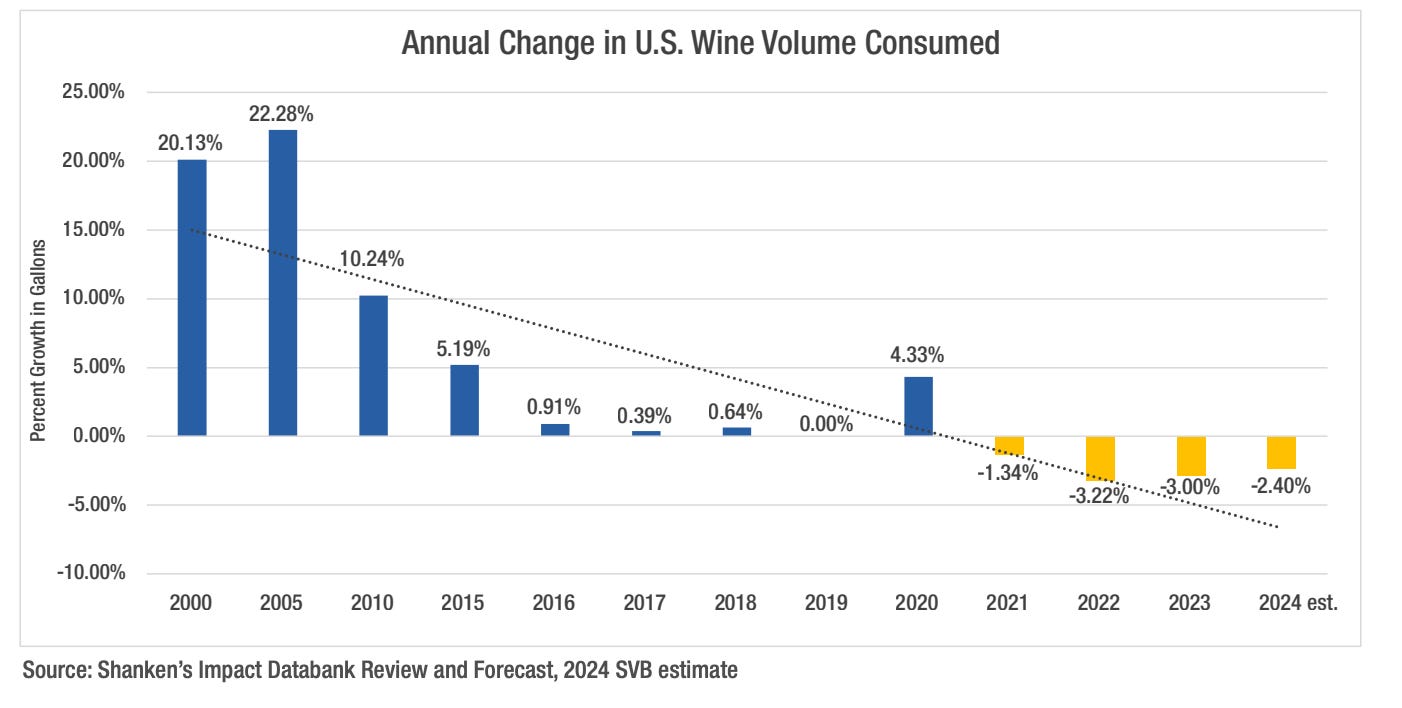

Wine has fundamentally struggled: the past few years have been difficult due to climate change, weaker production economics, decreased demand, and anti-trade policy. The combination of bad weather and higher costs on the supply-side has been met with added headwinds including policies like global tariffs and sustained lower consumption on the demand-side.

Though wine has decreased by about 5% this year as a store of value, it is not cheaper for consumers - restaurants and liquor stores have kept prices higher after sharp increases in 2022-23. Consumer price data implies retailers have hiked since. With alcohol PPI skyrocketing, who can blame them?

The considerable rise in menu prices over the past five years (est. 40-60% depending on location) makes ordering wine with dinner all the more maddening. Drinking a comparably priced bottle at home instead feels much better financially. In Manhattan for instance, one should be prepared to pay around $18 to 20 for a potentially mediocre glass - when $25 can buy a pretty decent bottle.

In any case, there may be relative value: purchasing high quality product directly from a producer, as policy and economics have created frictional costs across the supply chain. Investors benefit in the long term from buying cheap winners in a weak market backdrop.

September and October have been the first positive index growth months in years. While wine investments have underperformed precious metals and other commodity diversifiers, the tides may be turning for collectors and enthusiasts.

Improved ‘liquidity’

Technology makes prices more efficient.

Wine discovery used to be an iterative task - trusting friends and merchant picks, trying yourself, struggling to remember which ones you liked. Thankfully, online reviews have changed the game.

Tech companies like Vivino make the selection process significantly easier. Using your phone camera, their mobile app scans a bottle and displays reviews, sellers and prices. AI capabilities will only improve and create more features. Already, Vivino has crowdsourced enough data that their ratings are quite reliable.

From a theoretical lens, wider availability of information tilts the market in favor of higher quality wine, as buyers are more likely to choose top rated products. Plus, price efficiency increases when buyers see accessible sellers and prices transparently.

In terms of markets, wine/liquor auctions and exchanges have grown to a greater scale. Access to data and web APIs allow merchants and traders alike to derive and transact at accurate prices, mitigating painful price discovery. Though these sources are currently expensive, the stage has been set for lower information asymmetry. The ‘trading’ trend across e-commerce, betting, and financing of goods is a boon for wine merchants and collectors.

Undoubtedly, the decade has been marked by a spike in securitization and commoditization of various types of “assets” from NFTs to music royalty streams. Online platforms and marketplaces are engaged in a food fight for sector dominance. For wine, Liv-ex remains the leader, though high tech competitors are emerging.

At the end of the day, tech apps and market infrastructure make it easier than ever to buy and sell wine.

A turning point?

Hm…yes…a good year…splendid.

Persistent consumer trends include the popularity of rosé, white gaining share against red, Burgundy/Champagne/Italy regions remaining strong, and early prior decade favorites - Bordeaux and California - suffering most.

Younger vintages like ‘21, ‘23 and ‘24 are broadly regarded as weaker years compared to the high quality 2010s. The outlook for 2025 could be promising in regards to both quality and scarcity.

That said, bottle price appreciation is heterogenous2 and depends more on demand than “fundamentals” like quality - though scarcity definitely makes an impact.

Warmer global temperatures resulting in wildfires, droughts and heatwaves have made production quite complicated in recent years. Water shortages and rising energy costs add to these difficulties. Regions are subject to differing environmental challenges, but difficulties have broadly grown in magnitude.

Regions are also subject to political challenges. De-globalization and protectionist policies continue to stifle wine industry economics. Currency volatility does not help.

In the US, the Trump administration has shown a preference for Argentinian reds (technically violets3). US tariffs seriously threaten lower margin “commodity” wine producer businesses; they forced exporters to reroute shipments, prompted emergency export support and created short-term price volatility. While a few California producers hailed these tariffs, the majority are suffering due to higher import costs on key inputs like barrels from France and glass bottles from China.

Regulatory and compliance changes present structural pressure as well. New EU packaging frameworks raise costs and reporting obligations for bottle producers, shippers and importers. Meanwhile, the US is seeking to modernize wine labeling rules (proposed disclosures such as allergens and label approvals), meaning producers could face higher compliance and labelling costs in key markets alongside the political/trade uncertainty.

Ultimately, supply-side developments follow the societal trend of handing industries over to large operators with pricing power and greater economies of scale. Regardless, wine prices are primarily driven by demand. For one, demographic changes.

Aging and maturity

Millenials wining?

Fine wine is a long duration asset. It has an optimal drinking range, often around 10-20 years from the vintage. Hence its interest rate sensitivity. Historical correlation with other collectible luxury goods is highest, followed by rates.

The drinking population ages in tandem with wine. Millenials have recently been labeled the “drunkest” generation, especially compared to their younger cohorts. However, US preferences have been skewed towards hard seltzers and other ‘alternative’ alcoholic beverages, particularly amongst younger generations.

As consumers get older, wine typically becomes the beverage of choice. Boozy millenials are coming-of-age for a shift towards wine, while populous and wealthier older generations probably remain wine drinkers. Paired with increasing wealth inequality and a well-fed upper class, the bid for blue-chip booze could stay strong.

So long as drinking doesn’t fully go out of style…

Cheap or value trap

Buy now, drink later.

At this point, it is hard to say if fine wine and liquor is cheap or cheap-for-a-reason. Across data measurements, prices are affordable on a historical basis and negative momentum has slowed. Fundamental economics do not point to an imminent turnaround, but then again, prolonged periods of orderly selling can be good long term entry points.

Despite economic and political headwinds, fine wine and liquor provide actual consumption value that increases over time, compared to Labubu dolls or digital art. A bottle can lead to special memories or serve as a meaningful gift.

There are downside risks though. Alcohol consumption could continue to slide. Millenials could never adopt wine. Synthetic booze developed with AI could further disrupt the market. Weather, policies and regulations could worsen.

But buying consumer goods in a value trap has a positive side: even if the price grinds lower, you still bought it for cheap and can get value from it.

And on the other hand, global trade tensions could begin to relax. The legendary 2010s vintages still have a decent time horizon. Environmental and political factors could make high quality products rare. Consumer preferences are oscillating back towards more natural and organic products vs. artificial. There are real possibilities fading demand pivots.

Ultimately, strong arguments exist for both sides. The only certainty is that a correction occurred; the trend could continue, stagnate or pivot. Often though, corrections create opportunities. Wine does has intrinsic value and is cheap on both a historical and relative basis. Worst case - if you’re wrong, you can just drink it.

Though investment grade wine is less than 5% of the wine market, it does nicely measure overall value and directionality.

Wine collecting is very much a knowledge-based market with great individual vintages outperforming the pack. The Liv-ex Fine Wine 1000 index benchmark does not correlate much with broad “good years” while certain bottles and producers are big winners thanks to “good years”.

Javier Milei’s La Libertad Avanza party color is a violet purple.